The Ontario Housing Market is only getting tougher as the years pass by, with the average selling price of a home coming to $877,300 as of July 2024. It is even more expensive in Toronto with housing prices going more than $1,000,000.

Because of this, it can be daunting to buy your first home. After all, you have to account for a first time home buyer down payment, mortgage, and much more.

So, if you are a first time buyer in Ontario, you have come to the right place. Our real estate lawyer in Ontario has created a comprehensive guide for you to ease your burdens as a first time home buyer.

You can also go through our preliminary home buyer guide for Canada to help you understand what to expect.

First Time Home Buyer in Ontario Requirements

The top requirement for being a first time home buyer in Ontario is that you have never owned a home before, with the exception of divorce or separation or if you have received a home as an inheritance or gift.

If you are planning to opt for first time home buyer incentive and financial assistance, then you must have income below a certain amount to qualify.

There are various programs and incentives you can opt for, so keep on reading, as each one has a unique requirement as a first time home buyer in Ontario.

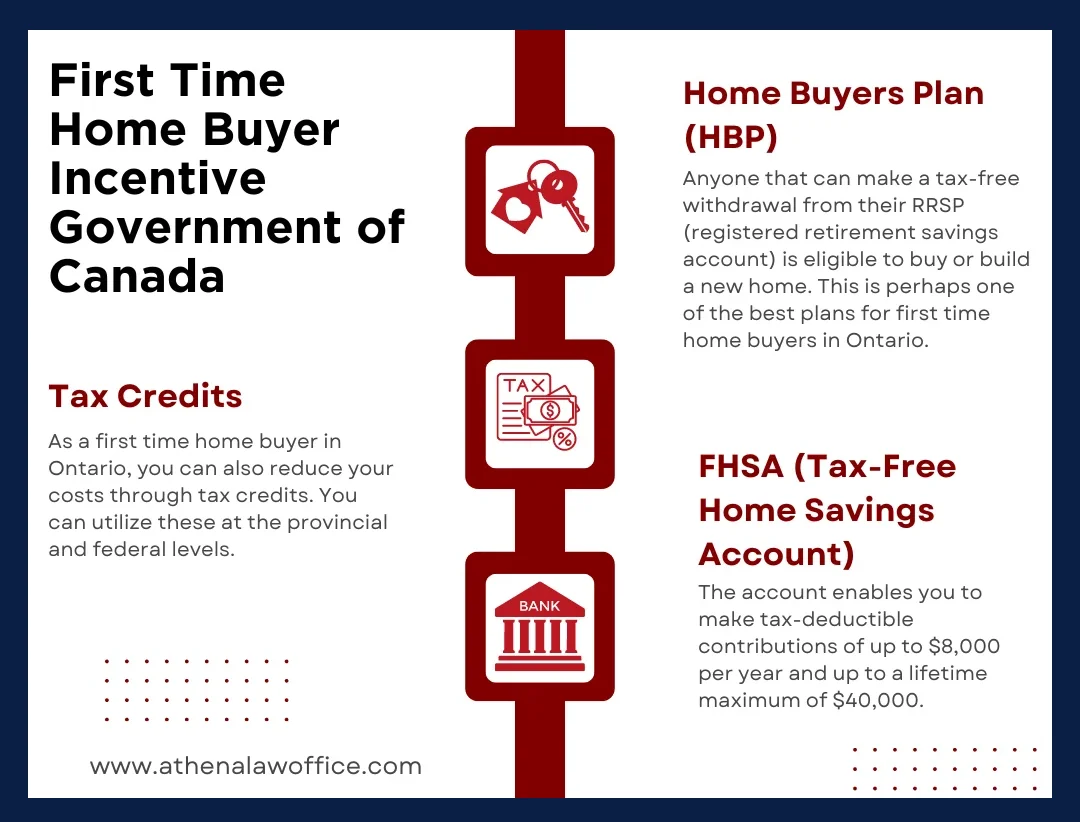

First Time Home Buyer Incentive Government of Canada

Here are some of the first time buyer incentives offered by the Government of Canada to help residents all over the country with buying a home:

1. Home Buyers Plan (HBP)

Anyone that can make a tax-free withdrawal from their RRSP (registered retirement savings account) is eligible to buy or build a new home. This is perhaps one of the best plans for a first time home buyer in Ontario.

This is because each individual can withdraw up to $35,000, which means if you are a couple, you can withdraw up to $70,000.

Then, you will have fifteen years to repay what you have borrowed. It will be interest-free, and repayment will begin two years after you have withdrawn the money.

Home Buyers Plan Eligibility

While the HBP is great for a first time home buyer in Ontario, the program is also ideal for people who have been separated or divorced. Since 2020, separated or divorced people can also take advantage of the HBP even if they are not first-time home buyers.

So, if you are separated or divorced, you can use the HBP a second time to purchase a new home or buying out your ex-spouse’s share of the property. However, you can only avail this if your first HBP withdrawal has been repaid completely.

If you want to buy or build a home for someone related to you with a disability or help them buy or build a home, then you can also be eligible for HBP. The only caveat is that you must have the intention that the person with the disability will occupy the home as their primary place of residence.

You can understand the Home Buyers Plan in detail here.

2. Tax Credits

As a first time home buyer in Ontario, you can also reduce your costs through tax credits. You can utilize these at the provincial and federal levels.

Here are the two types of tax credits you can use to buy a home:

Home Buyer’s Amount

You can utilize the home buyer’s amount to decrease your taxes in the year you are purchasing a home as a first time home buyer in Ontario. However, you will only be eligible if:

- You and your spouse or common-law partner purchased a qualifying home with the intention to live in it. Or with the intention of a related person with a disability occupying the home as their primary residence.

- You have not lived in another home that you or your spouse or common-law partner owned during the year you purchased it or in any of the four preceding years from the purchase.

Please note that you can only use these credits for a qualifying home. These include condos, prefabricated homes, townhouses, semi-detached homes, single-family homes, mobile homes, apartments in built-unit residential buildings, or ownership in a housing co-op that provides you with an equity interest.

Housing Rebates

This is only applicable to some of the provinces if you are a first time home buyer. For example, if you are a first time home buyer in Ontario, then you can get a rebate on your land transfer taxes.

In other provinces, individuals who co-own a new or substantially renovated home can benefit a from a partial or full tax rebate. The only caveat is that the home must be used as the primary residence of the buyer or one of their relatives.

3. FHSA (Tax-Free Home Savings Account)

The FHSA is a tax-free account that will help you save for your first home. The account enables you to make tax-deductible contributions of up to $8,000 per year and up to a lifetime maximum of $40,000.

As soon as you open your first FHSA, your contribution room will begin to accumulate. You can also use your unused FHSA contribution room, up to a maximum of $8,000, in the coming year as a first time home buyer in Ontario.

FHSA Eligibility

If you want to open an FHSA, then you will have to meet the eligibility criteria, which includes the following:

- You must be between the ages of 18 and 71

- You should be residing in Canada

- You must be a first time home buyer in Canada

You will also be relieved to know that you can transfer your funds from RRSP to FHSA without paying any taxes. However, the contribution limit is $8,000 per year, with a lifetime limit of $40,000.

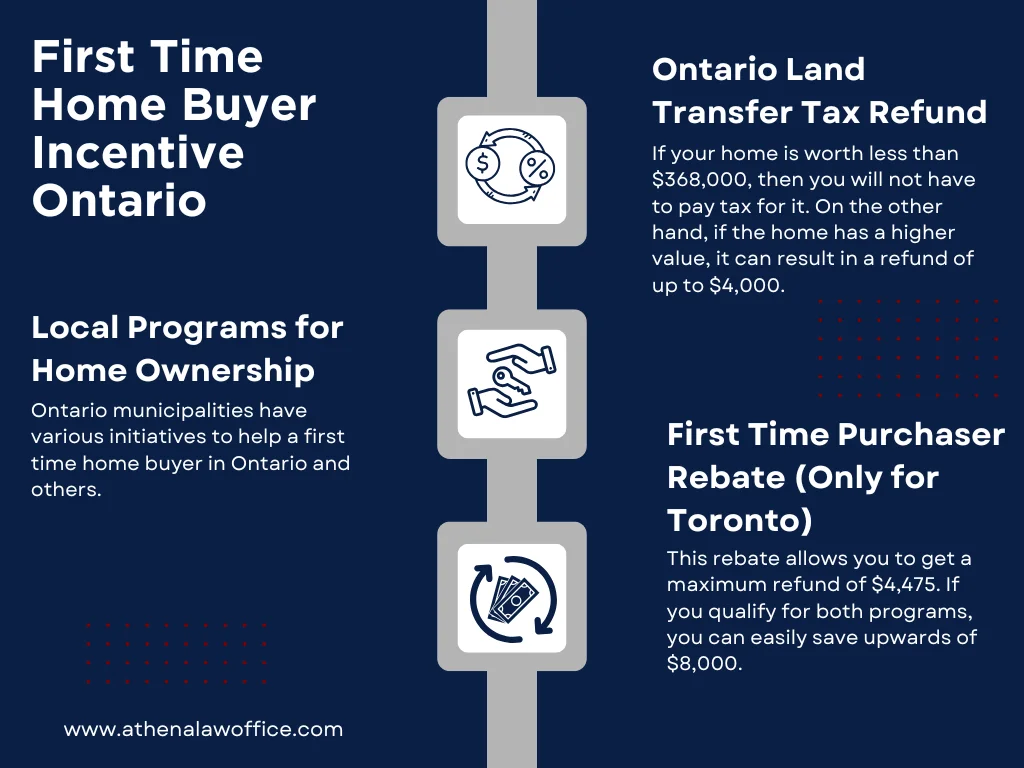

First Time Home Buyer Incentive Ontario

Here are some incentives for first time home buyers specific to Ontario. If you live in this region, you can benefit from these incentives as a first time home buyer in Ontario:

1. Ontario Land Transfer Tax Refund

A first time home buyer in Ontario is eligible for the Ontario Land Transfer Tax Refund. This is one of the top standard closing costs in Ontario that you can avoid when purchasing a home for the first time.

If your home is worth less than $368,000, then you will not have to pay tax for it. On the other hand, if the home has a higher value, it can result in a refund of up to $4,000.

Here is the eligibility criteria for the Ontario Land Transfer Tax Refund:

- You must be a permanent resident or citizen of Canada

- You must be at least 18 years old

- After registering the home in your name, you must live in it as your principal residence within nine months

You can also consult a real estate lawyer in Ontario to determine the refund you will receive on the home you plan to purchase.

2. Local Programs for Home Ownership

Ontario municipalities have various initiatives to help a first time home buyer in Ontario and others. Please note that even if you are not a first time home buyer in Ontario, you can still benefit from these initiatives if you meet the eligibility criteria.

These are some of the top local homeownership programs in Ontario that can assist you with buying your first home:

| Program | Assistance Type | Amount | Eligibility Criteria |

| Simcoe County | Down payment loan | 10% of the purchase price with a maximum purchase price of $593,879 | Must be renters with a gross household income of a maximum of $103,200 |

| Waterloo Region | Down payment loan | 5% of the purchase with a maximum price of $506,000 | Maximum household income of $101,300 with residing in Waterloo for the last twelve months |

| Chatham-Kent | 20-year interest-free loan | 10% of the purchase price with a maximum purchase price of $250,000 | Gross household income of $95,000 |

| Kingston | Forgivable loan | 10% of the purchase price with a maximum price of $440,000 | Renter household with a pre-tax income lower than $94,000 |

| Muskoka | Down payment loan | 10% of the purchase price with a maximum price of $726,600 | |

| Dufferin County | Interest-free loan | 10% of the purchase price with a maximum price of $609,118 | Income at or below $109,000 or $132,000 for two or more earners. Maximum assets of $30,000 |

| Brantford | Forgivable loan | 5% of the purchase with a maximum price of $400,000 | Current renters in Brant County or Brantford with a gross household income below $90,600 and assets worth less than $30,000 |

3. First Time Purchaser Rebate (Only for Toronto)

If you are a first time home buyer in Toronto, then you avoid the municipal land transfer tax partially or completely. Please note that the requirements of Ontario’s provincial rebate program will also apply here.

This rebate allows you to get a maximum refund of $4,475. If you qualify for both programs, you can easily save upwards of $8,000.

Tax Incentives for Homeowners in Canada

Owning a home can lead to various financial difficulties, and the Government of Canada understands this. So, to offset these difficulties, the Canadian Government provides various tax incentives for a first time home buyer in Ontario and other provinces.

These incentives are for first time buyers and anyone else that wants to buy a home. Here are the top tax incentives for you to choose from:

Home Accessibility Tax Credit (HATC)

The HATC is a tax credit for renovations to make the home accessible for people with disabilities. It is non-refundable and must be used to allow a person to be more functional or mobile within the home and reduce the risk of injury or harm.

If you qualify for this tax credit, you will have an annual expense limit of $20,000. So, be sure to check your eligibility.

MHRTC (Multigenerational Home Renovation Tax Credit)

Anyone who wants to live with other family members in the same home can opt for MHRTC to make the process more affordable. You will receive a refund for eligible expenses.

You can claim up to $50,000 for each renovation that qualifies for the tax credit. You can claim this with a credit of 15% of costs, and a maximum limit of $7,500 for each claim.

First Time Home Buyer Incentive: Is It Discontinued?

You might have heard of the first time home buyer incentive by the CMHC (Canada Mortgage and Housing Corporation). However, it has been discontinued from March 2024.

The incentive helped an eligible first time home buyer in Ontario to reduce their monthly mortgage payments without increasing their financial burdens. It was a shared equity mortgage with the Canadian Government.

The deadline for new submissions was March 21, 2024, and no new applications will be taken or approvals granted after March 31, 2024. So, if you are a first-time home buyer in Ontario, this incentive is not an option for you anymore.

First Time Home Buyer in Ontario Down Payment

When you decide to buy a home in Ontario, it is crucial to investigate your mortgage options and the down payment needed for potential homes you want to buy.

Typically, across the country, you will need to provide between 5% and 20% of the purchase price as your down payment.

On the other hand, if your down payment is less than 20%, then you will need mortgage loan insurance, which can be anywhere between 0.5% and 4.5% of the mortgage amount.

Tips for First Time Home Buyers in Ontario

Now that you are familiar with the process of home buying, it is good to follow some rules when you are a first time home buyer in Ontario. These tips will allow you to get the most out of your investment, and shop for the best home.

Here are the top tips for a first time home buyer in Ontario to add to their home buyer’s checklist:

1. Research the Local Region of the Property

While real estate news will catch you up with regional trends, it is more important to keep a check on the local activity where you are planning to purchase your first home.

You can opt for a real estate lawyer or agent who specializes in that region to help you purchase your first home. For example, if you live in Scarborough, then you can opt for Athena Narsingh, a real estate lawyer in Scarborough to help you with the process.

We also recommend doing some research on it yourself to understand whether it would even be a good investment for you in the long run. For more information, you can connect with our real estate lawyer.

2. Set a Budget

Houses are expensive, and as a first time home buyer in Ontario, you must set a realistic budget for yourself with an upper limit. Your finances and income will determine the type of house and neighborhood you can live in.

There are various costs to consider based on your region. For example, in Ontario, you must take into account closing costs, real estate lawyer fees, land transfer tax, and much more.

You must also set aside some money for renovating and upgrading the house after you move in.

3. Check Federal and Local Programs for First Time Home Buyers in Ontario

Canada has federal programs for home buyers and Ontario has local programs for its residents. We have already discussed these in detail above.

We recommend you go through each of these programs and then decide what will work best for your home buying circumstances and needs.

4. Scour Home Insurance Options

Home insurance in Ontario is also incredibly important in protecting your asset. If you are a first time home buyer in Ontario, you must scour your options to find the right policy for your home.

Here are a few things about home insurance in Ontario you must look into before choosing the best one for your needs:

- Coverage of the policy

- The type of policy that will work best for you

- Seeing if you can bundle home insurance policies with others to benefit from discounts

- Look for deductibles that suit your financial circumstances

These are just some of the things that will aid you in selecting the right home insurance policy in Ontario. As a first time home buyer in Ontario, you can contact an experienced real estate lawyer to help you select the best options.

5. Talk to a Mortgage Broker

You will need to know the mortgage amount you can qualify for and what your monthly mortgage payment will be. This will help you understand your budget and the purchase price you can afford.

Here is a sample of what types of monthly expenses you can incur:

| Mortgage | $1958 |

| Maintenance | $210 |

| Hydro | $150 |

| Waste Management | $80 |

| Property Tax | $167 |

| Home Insurance | $150 |

| Internet | $80 |

| Groceries | $500 |

| Cell Phone | $130 |

| Car Insurance | $120 |

| Life Insurance | $145 |

| Medical Insurance | $200 |

| Gas | $200 |

| Total | $4090 |

6. Find the Right Home

Once your finances are sorted as a first time home buyer in Ontario, contact your real estate agent and start the hunt.

Here are some tips on picking the right agent:

- Talk to your potential agent and tell them what you are looking for as a first time home buyer in Ontario.

- See if you and your agent can “click” and have a relationship. Sometimes you can find your dream home after the first showing, other times, you may be looking for over a year. It is important to have a good relationship with your agent.

- Do not sign a commitment with them unless you are sure this is the right agent for you.

- Make a list of questions you want to ask your agent to make sure they understand you.

Here are some tips on picking the right home:

- Figure out what you want in a house (open concept, three bedrooms, two bathrooms, backyard, etc.)

- Determine what are your “must haves” and what you are willing to negotiate.

- If you don’t know what you want in a house, check out a few different types of houses and look up inspirations online.

- Determine what city you want to live in. Consider if it is close to your work, nearby schools, family, etc.

7. The Final Process

So you have found your dream home and put down a deposit as a first time home buyer in Ontario. What happens next?

- Get a real estate lawyer. The fees will be a flat rate plus disbursements. Expect to pay around $2000 in total.

- Confirm your mortgage with the bank and provide them with your lawyer’s contact information.

- Your lawyer will ask you for documents to complete the forms for you to sign. These forms will be done. Some forms will be for the bank.

- The lawyer will then meet with you to sign the forms, which they will then submit to the bank.

- The bank will then confirm they will provide the mortgage funds to the lawyer.

- A few days before the closing, you will deposit the remainder of the downpayment to the lawyer’s trust account or drop a certified cheque at their office.

- On the day of closing, the seller’s lawyer will send signed documents from the sellers. Your lawyer will receive the mortgage funds and deposit a cheque to the seller’s lawyer. Then, they will register the property in your name electronically.

- Lastly, the lawyers will exchange the keys or give a lockbox code.

- This closing can occur between 12 p.m. and 5:00 p.m. Your lawyer will update you throughout the day.

FAQs

Who qualifies for first time home buyer in Ontario?

Anyone who has not occupied a home they own or one that their current spouse or common-law partner owned in the last four years.

The amount is up to $4000 for each land transfer tax applicable to your city. For example, there are two land transfer taxes in Toronto, and another for Ontario. The total rebate is up to $8000.00.

The amount of the rebate depends on how many owners qualify for the rebate. For example, if there are three home buyers, and one qualifies for the rebate, the amount eligible is $1,333.00 if the property is not in Toronto.

Are they getting rid of first time home buyer incentive in Ontario?

Yes, the first time home buyer incentive in Ontario has been discontinued by the CMHC (Canada Mortgage and Housing Corporation). The deadline was March 21 2024, and now no new applications are being taken.

What is the first time home buyer incentive in Canada?

The first time home buyer incentive in Canada was a program where the government provided 5 to 10% of the home’s price, depending on the type of the home. You can think of it as a second mortgage on the home, but this incentive has been discontinued.

What is the minimum down payment for a house in Ontario?

If the purchase price is less than $500,000 then the minimum down payment for a house in Ontario is 5%. On the other hand, if the purchase price is between $500,000 and $999,999. Then, the minimum down payment is 5% on the first $500,000 and 10% on the remaining amount.

Contact Our Real Estate Lawyer in Scarborough for a Free Consultation

Now that you understand the important basics as a first time home buyer in Ontario, it is crucial to have the right kind of help by your side. The first step is getting a real estate lawyer to help you with everything you need.

For more information, you can connect with Athena Narsingh, a trusted and knowledgeable real estate lawyer in Scarborough, to help you through the process of buying a home as a first time home buyer in Ontario.

Author Profile

- Barnett Law is a trusted and knowledgeable lawyer in Scarborough. Her expertise spans real estate law, family law, adoptions and fertility law. A lawyer by profession and a humanitarian by heart, Athena Narsingh Barnett wants to help people become more familiar with the legal system and be well-informed to make important legal decisions.

Latest entries

Real Estate LawJanuary 30, 2026Non Resident Speculation Tax Explained For Beginners

Real Estate LawJanuary 30, 2026Non Resident Speculation Tax Explained For Beginners legal guidanceNovember 12, 2025How To Avoid Land Transfer Tax Ontario?

legal guidanceNovember 12, 2025How To Avoid Land Transfer Tax Ontario? legal guidanceOctober 31, 2025How Much Is Land Transfer Tax In Ontario?

legal guidanceOctober 31, 2025How Much Is Land Transfer Tax In Ontario? Family LawOctober 27, 2025How Much Does A Divorce Cost In Ontario In 2025?

Family LawOctober 27, 2025How Much Does A Divorce Cost In Ontario In 2025?